Americans have been through a tough few years, but I am optimistic about our country’s economic prospects. Americans’ resilience has helped us recover from the economic crisis created by the COVID-19 pandemic, families are finally getting more breathing room, and my economic plan is making the United States a powerhouse for innovation and manufacturing once again.

In the list of economic accomplishments, I could find no mention of housing. None. Zero. There could be a few reasons for this:

There is little good news on the housing front.

The new about housing is less good or clear than the areas Biden cites.

Housing is not viewed as a winning political topic.

What could political leaders do to help deliver a Christmas housing present for Americans? How can they talk about jobs, incomes, taxes, and opportunities without mentioning one of the most basic pieces of the good life in the United States: a pleasant home or residence in a decent location?

I keep thinking about the car commercials that have run for years featuring people getting new cars, SUVs, or trucks as Christmas gifts (sometimes with a bow). This might be the ultimate in Christmas consumption: a true big ticket purchase on the biggest consumer day. At the same time, Americans like cars and driving and are willing to shell out for it. Americans also like single-family homes; could someone develop a Christmas housing share gift program? Or, “give a mortgage”?

What’s going on? One problem is simply with the shape of office buildings: Their deep floor plates mean it’s hard for natural light to reach most of the space once it’s divided up into rooms. Their utilities are centralized, which requires extensive work to bring plumbing and HVAC into new apartments. Either way, they require significant architectural intervention. The older stock of prewar offices, which are better suited for residential units, have often already been converted in cities like Chicago and Philadelphia. Another issue is with zoning codes that bar housing from office districts. A third obstacle is the building code: Early residential conversions, like those in SoHo’s lofts, were usually illegal, sometimes for complicated reasons that seem less important than mandating a window in every bedroom.

What’s more, business districts don’t empty out building by building but with vacancies here and there across the skyline. You wouldn’t convert Twitter’s building, since it’s partially occupied by workers. So, in one sense, Musk’s bed stunt is an example of his already innovating at Twitter. Very mixed-use! “You’re not going to run into a building that’s 100 percent empty, ready to be converted,” said Anjali Kolachalam, a researcher with Up for Growth. She recently ran office space in downtown Denver through a filter to find good conversion targets—tall buildings with high vacancy rates and small floor plates built before 2010. She wound up with just 4 office buildings, out of the 208 total.

Finally, converting buildings to residential use is expensive. Couple that with the fact that office rents are higher per square foot than residential rents are, and you see why developers aren’t champing at the bit to get new projects underway. Van Nieuwerburgh gave me an example from San Francisco, where Juul’s old headquarters—down the block from Twitter’s improvised dormitory—is for sale for $150 million. That’s a lot less than the $397 million the embattled nicotine vape company paid for it in 2019. But at $400 a square foot to buy and another $400 a square foot to renovate, he said, the conversion would still produce a building with rents too high even for San Francisco. In other words, offices may be down, but they’ll have to fall a lot further before adaptive reuse becomes a bargain.

While the challenges are present, I wonder if someone has this figured out – this could be a company, developer, or community. Are there ways to quickly address the issues listed above or does it require a sustained effort? Imagine someone figures this out and there is a way to make some cool conversion from an exciting work space (if this is possible) or name to an interesting housing unit. If this can happen for churches and religious buildings, why not for office buildings?

If this does not work easily now, could we anticipate new buildings that could more easily switch between uses? There are ways to plan, zone, and build with more flexibility in mind so that adjustments could be made given needs and market conditions. Would it cost more to construct a building in this way? If so, perhaps the possible higher occupancy rates and the ability to adjust could bring in more money in the long term.

Looking at the number of American households and the number of vacant housing units, Freddie Mac, the government-sponsored purchaser of mortgage-backed securities, estimates a current supply shortage of 3.8 million units, driven by a 40-year collapse in the construction of homes smaller than 1,400 square feet.

The group Up for Growth also arrived at an estimate of 3.8 million, using data on the total demand for housing and the overall supply of habitable, available units.

The National Association of Realtors compared the issuance of housing permits with the number of jobs created in 174 different metro areas. It found that only 38 metro regions are permitting enough new homes to keep up with job growth; in more than a dozen areas, including New York, the Bay Area, Boston, Los Angeles, Honolulu, Miami, and Chicago, just one new home is getting built for every 20-plus jobs created. The NAR estimates an “underbuilding gap” of as many as 7 million units.

These numbers draw on data such as vacancy rates, household-formation trends, and building trends. But none of the estimates capture what I’ve come to think of as the affordability gap: the difference between the housing we have and the housing we would need in order to ensure that working-class people could once again live in our big coastal cities for a reasonable cost. Freddie Mac does not purport that building 3.8 million units would make New York accessible to big middle-class families and end homelessess in San Francisco. The National Association of Realtors is not contemplating whether janitors can walk to work in Boston…

To come up with that estimate, the two economists built a complicated model that assumed Americans could move wherever their wages allowed and the housing supply would adjust as it would in a place with typical permitting standards. In such a world, they estimated in some associated work, 53 percent of Americans would not live where they are currently living. San Francisco would have an employed population 510 percent bigger than it does today—implying an overall population of something like 4 million, rather than 815,000, with 2 million housing units instead of 400,000. The Bay Area as a whole would be five times its current size, the economists estimated. The average city would lose 80 percent of its population. And New York would be a startling eight times bigger. Some back-of-the-envelope math (mine, not theirs) suggests that the United States would have—deep breath here—perhaps 75 million more housing units in its productive cities than it currently has.

Considering such big numbers can be both helpful and daunting. The sheer size of these figures – multiple millions to tens of millions – highlights the scope of the problem. Housing is not a small issue; it is a large issue that needs addressing. Big numbers can help convince people this is an important social issue to address. On the other hand, these figures are daunting. That is a lot of housing units to consider. How can small efforts contribute to such a big need? Who can address this?

Even if the various methods and experts above do not agree on the same numbers, together they suggest much needs to be done. Can we get a commitment from states or cities to approve more units proportionate to their populations? I could imagine some kind of pledge drive and counting system to see the progress toward a sizable goal. Or, how about a long-term plan on the scale of a Manhattan Project or a space race to get units built? Of course, addressing housing at the federal level is difficult.

In housing circles, one hears a lot of self-righteous discussion about the need for more preservation. And many American homes doubtless deserve to stick around. But the truth is that we fetishize old homes. Whatever your aesthetic preferences, new construction is better on nearly every conceivable measure, and if we want to ensure universal access to decent housing, we should be building a lot more of it…

In the meantime, we’re stuck with a lot of old housing that, to put it bluntly, just kind of sucks. A stately Victorian manor in the Berkshires is one thing. But if you live in a Boston triple-decker, a kit-built San Jose bungalow, or a Chicago greystone, your home is the cheap housing of generations past. These structures were built to last a half century—at most, with diligent maintenance—at which point the developers understood they would require substantial rehabilitation. Generally speaking, however, the maintenance hasn’t been diligent, the rehabilitation isn’t forthcoming, and any form of redevelopment is illegal thanks to overzealous zoning.

You might think uneven floors or steep stairwells have “character.” You’ll get no argument here. But more often than not, old housing is simply less safe…

The fact is that those much-lamented cookie-cutter five-over-one apartment buildings cropping up across the U.S. solve the problems of old housing and then some. Modern building codes require sprinkler systems and elevators, and they disallow lead paint. New buildings rarely burn down, rarely poison their residents, and nearly always include at least one or two units designed to accommodate people in wheelchairs.

And despite what old-home snobs may believe, new housing is also just plain nice to live in—in many ways an objective improvement on what came before.

New housing does indeed have features, including aesthetic choices and functionality, that often better suit current users. Safety can be a persuasive argument. And there certainly is a need for more housing units in many locations.

However, continuing to use, rehabbing or renovating, and preserving housing can sometimes address these concerns and provide continuity in structure and character. We often tie concepts like stability, tradition, and permanence to housing units, even if they are not the best construction or something better comes along later.

What would be interesting to see is if one American city or region was willing to commit to building new housing in the way described in this piece. If there is there is the will and resources to construct plentiful, attractive, and safe new housing and not fix up or save older homes, what would happen?How would it transform everyday life and society?

One aspect of this debate that I wondered about: is it greener to build a lot more new housing or to rehab existing housing?

When it comes to housing, it might be better to think about the U.S. as a country of 384 metro areas (plus 50 million Americans who don’t live in places big enough to qualify as a metro area) rather than one continuous country. In 2021, the U.S. population grew just 0.1% – the lowest annual expansion rate since our nation’s founding. But housing dynamics are best viewed through the different metro areas that are growing and shrinking. Of the 384 metro areas, 72 had declining populations in the decade leading to 2020, according to the Census.

The general argument makes some sense: supply and demand for housing depends on the metropolitan region. I have lived in one of these regions that has very limited demand for housing and experienced numerous foreclosures in the late 2000s. In places such as these, housing is cheap and plentiful – but there are relatively few people who want to move there and, if they do, there is limited desire to rehab older homes. On the other hand, the activity in particular housing markets – such as the coverage of housing and population in Manhattan and San Francisco during COVID-19 – draws all sorts of attention because of the prices and demand. All of this contributes to why housing is difficult to address at a national level.

More broadly, seeing the United States as a collection of metropolitan regions (or expanded citystates?) may make some sense. For example, the 9+ million people in the Chicago region may see themselves as more of a collective than describing people from Illinois or people from the Midwest. These people share a particular housing and jobs market, common sources of information, entertainment options, a transportation network, and regional forces.

Of course, some regions may be more like other regions. Scholars have examined some of these broader collections, such as Rust Belt or Sunbelt regions or immigrant gateways, or used particular cities as models – particularly Chicago, New York, and Los Angeles – by which we can better understand all cities and regions. Yet, even these regions that share common characteristics have particular histories and current realities that would help set them apart from other.

All of this gets at an ongoing issue in sociology and other disciplines: at what point is it worthwhile to group phenomena together because of common traits or is it better to leave them as distinct entities because of their differences? There are both common traits in and a lot of variation among the 384 metro areas (plus all the other people living outside metro areas). At least for housing, it is tempting to treat each market as unique even as there are common patterns.

Del Webb of Sun City fame recognized that, rather than rocking away their “golden years” in the northern cold, older adults could be convinced to pull up roots, leave empty nests and move to communities of similar people and lives of leisure. A radio jingle promoting this new model of living sang out: “Don’t let retirement get you down! Be happy in Sun City, it’s a paradise town.”

But is a town without the sounds of children and a diversity of races and styles really a paradise?

A growing number of older adults say no, recognizing that living with neighbors of all ages and from all walks of life just makes sense. They realize that intergenerational connections are not just valuable for them but for their communities and country.

They recognize that ageism will not be defeated by a retreat to age-segregated corners, but only by engagement, collaboration and dialogue across age, race and class divides. They believe that there is more to graying than playing.

This commentary also hints at a broader issue in the United States: why is aging treated as it is? Why aren’t older adults seen as resources rather than liabilities? Why aren’t intergenerational relationships and communities celebrated more? These communities might be considered the physical embodiment of particular cultural values in the United States.

The share of mortgage borrowers in forbearance programs fell below 4% as of June 8, the lowest level since the onset of the Covid-19 pandemic, according to Black Knight Inc., a company in Jacksonville, Fla., that provides data and software to mortgage lenders and servicers…

In August, Census projected that there were 1.7 million American adults living in households that weren’t current on their mortgage payments and who thought it was very or somewhat likely that they would lose their homes in the next two months. By just before Christmas that was up to 1.9 million. It fell to 1.2 million by March and was around 900,000 in the latest survey covering May 26 to June 7.

The trend is similar for renters. In August Census projected that there were 3.8 million American adults living in households that were behind on the rent and who thought it was very or somewhat likely that they would lose their homes in the next two months. Just before Christmas the total was 5.2 million. It dropped to 3 million in March. In the latest period it edged back up to 3.2 million.

This is still a large number of people and there are additional concerns:

That’s not to say all is well. Many people fall through the cracks. In an analysis of the latest Census data, the Center on Budget and Policy Priorities says that one in five renters in households with children were behind on the rent as of the May 26-June 7 survey. There are also disparities by race. While 10% of non-Latino White households were behind on the rent, 16% of Latino households and 24% of Black households were behind on the rent.

COVID-19 helped bring to the forefront the issue of housing facing many Americans. On one hand, someone could say that COVID-19 was such an unusual event that affected so many jobs. On the other hand, there are other social changes – think automation or the decline of major sectors in the economy – that could also affect the ability for many Americans to find and keep decent housing. Add to this the other oddities of the COVID-19 housing market, including those with resources could leave cities and the limited supply of housing, and there are numerous issues to consider.

More broadly, this offers an opportunity to discuss housing in the United States. Should people be afraid for their housing in a time of crisis? Where is more affordable housing going to come from? What should landlords, builders, and investors expect in times of economic trouble? Is housing itself a primary driver in the inequality in wealth and access to housing? How much should income be tied to the quality of housing?

These are not new questions but perhaps ones that are more pressing in light of current events. Of course, addressing housing at a national scale is not easy. Yet, the number of people still in a housing lurch in the coming months might help move the conversation on housing forward.

The world’s second biggest country by landmass is effectively running out of space, and that has Canada on course for a reckoning. The dream of a detached home and a piece of land, which generations of Canadians have taken for granted, and which continues to entice new immigrants, may soon be out of reach in the places where people want to live. That could force an expansion of the idea of home to include condos and rentals, potentially transforming how the middle class does everything from raising families to saving for retirement…

In Canada, buying a home has long been seen as the surest path to middle class security. Canadians on average live in some of the biggest houses in the world, and post higher rates of homeownership than in the U.K., or France, or even the U.S. The pandemic has put an even bigger premium on backyards and extra space…

Still, developers don’t seem to be responding. Though construction started on a record number of new homes in Canada’s metro areas in March, the percentage that were single family-detached actually fell to 19% from 24% the previous year, according to government data. While this ratio improved in April, new home starts slowed that month overall…

It comes down to land. While Canada boasts a total area of about 10 million square kilometers (3.9 million square miles), roughly 40 times the area of the U.K., most Canadians are clustered in a handful of major cities not far from the U.S. border. That’s where the jobs are. And while the work-from-home era has expanded that radius for some, turning quiet farming communities and weekend-getaway spots into the hottest real estate markets in the country, the possibility of returning to the office even a few days a week has kept most workers from striking out too far afield.

The proposed solution in the article is more condos, apartments, and townhouses. These would have provide denser populations and expand the housing options. But, this is not what all Canadians want: like in the United States, the idea of a single-family home is both popular as an ideal and investment.

Here is a different answer from Canada’s southern neighbor: sprawl. More and more sprawl. The article says Canada is out of land; this is not quite true. Keep building suburban areas out from cities. Take advantage of the work from home days of COVID-19. Build on the interest of some Canadians to have their own home and land. Give in more to car culture. Go thirty, forty, fifty miles out like the biggest American cities. There will still be plenty of land in the middle of the country for farms and up north for open space.

This may not be a welcomed answer. This all leads to more driving, more dependence on roads. It means less energy efficiency, perhaps particularly during cold winters. It might introduce the same problems that plague sprawling American metropolitan areas.

But, if Canadians do not adjust to living in smaller units in closer proximity, sprawl is one option. The emphasis on homeownership and vehicles is already there. It could be a different kind of sprawl, maybe denser than the American version or more community oriented. Perhaps some lessons could be learned from the mistakes made in the United States. At the least, it could relieve some housing pressure, provide jobs for builders and developers, and set up new subdivisions and future communities for decades to come.

What’s missing? The low-rise, multifamily housing that the city banned in the 1970s and ’80s. Which is why Christopher Hawthorne, the city’s chief design officer, held a competition, “Low-Rise: Housing Ideas for Los Angeles” to solicit new blueprints for so-called “missing middle” housing. “There’s a narrative in L.A., as in many cities, that neighborhoods are changing too fast; but in reality, L.A. is changing less rapidly than at any point in its history,” Hawthorne told me. A former architecture critic at the Los Angeles Times (and for this magazine), he plans to use these designs to win hearts and minds in the community forums where upzoning goes to die.

The winning entrants, announced on Monday, are a reminder that multifamily housing does not need to look much different than single-family housing. Instead, these models weave apartments right into the neighborhood, with understated architecture and clever use of space. In theory, these modest plans ought to take the “neighborhood character” argument against housing growth off the table.

Then again, the whole dialectic of NIMBY vs. YIMBY, Hawthorne contends, doesn’t accurately describe the situation on the ground. “When we actually talk to communities and neighborhoods, we find most people are in the middle. A lot of recent scholarship has clarified historic issues”—such as single-family zoning’s legacy of racial exclusion—”pandemic and wildfire have clarified others. Most people are ready to say our approach of land use and zoning in low-rise neighborhoods is not a sustainable pattern for the 21st century.” They just need help visualizing what change looks like.

There are multiple layers of issues present in these three paragraphs. Here are a few of the issues as I see them:

There is a continuum of change within a neighborhood ranging from frozen in time for decades to immediate massive change in a relatively short amount of time (perhaps in urban renewal style after World War Two). All communities change to some degree but this is affected by time, demographics, and other factors. I wonder how effective it is, as above, to note the relative lack of change to people in a neighborhood who might perceive it differently. I cannot quantify it but I would guess there are plenty of people who move into a location and expect it not to change (or only change in ways that they approve).

The change in character, often equated with adding anything different to single-family homes of the same kind, is hard to combat. Perhaps more people see the need for more housing but how many want it on their block or immediate area as opposed to somewhere else in the city?

I agree that design can help ameliorate these issues. It might be worthwhile to build one of these options with no one’s knowledge and then see who notices. There are ways to construct affordable or even subsidized housing in ways that do raise the attention of nearby residents who might otherwise oppose any efforts to have cheaper housing.

How much would local politicians push for these changes as opposed to representing the existing residential interests? This could matter less if local politicians are at-large representatives but this would also raise the ire of particular neighborhoods.

Neighborhoods with more resources – higher-income residents , people with more connections to politicians and community groups – may be able to slow down or delay possible change more than others. And if the new housing might bring in people not like them, the race/class/”others” issues could be more at play than any actual debate about housing options.

How much change in a neighborhood or character change is desirable? It could vary from community to community and depend on numerous factors.

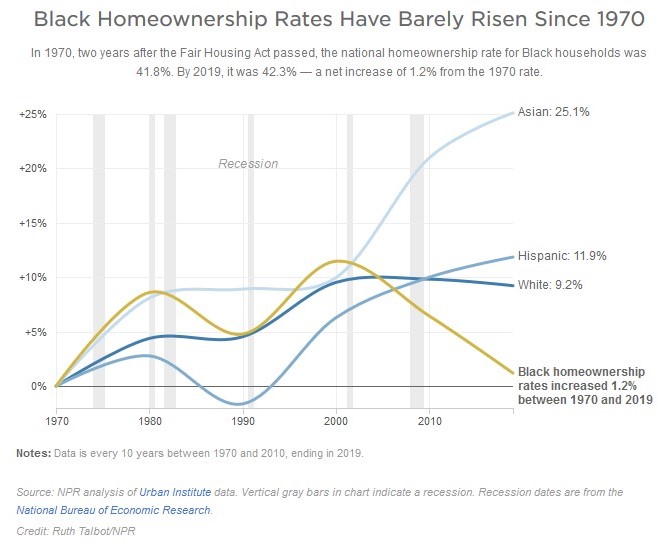

After this chart at the top, the rest of the article is an in-depth look at race, lending, and housing in the Los Angeles area. While some of the story involves factors pre-1960s, there is also much after the Civil Rights Movement that has limited homeownership. All groups on the chart had higher homeownership rates into the early 2000s but conditions changed for Blacks such that they experienced a decline.

All of this makes the recent efforts in Evanston, Illinois, just north of Chicago, all the more interesting. The discussions of reparations there have settled on providing funds for housing. From the City of Evanston FAQs:

In July 2019, the Equity and Empowerment Commission held community meetings to solicit feedback from community members on what reparations would look like for the City of Evanston. Affordable housing and economic development were the top priorities identified during those meetings. A report was submitted to the City Council for consideration and was the basis for Resolution 126-R-19, “Establishing the City of Evanston Reparations Fund and the Reparations Subcommittee.”

Reparations, and any process for restorative relief, must connect between the harm imposed and the City. The strongest case for reparations by the City of Evanston is in the area of housing, where there is sufficient evidence showing the City’s part in housing discrimination as a result of early City zoning ordinances in place between 1919 and 1969, when the City banned housing discrimination.