What drives these differences?

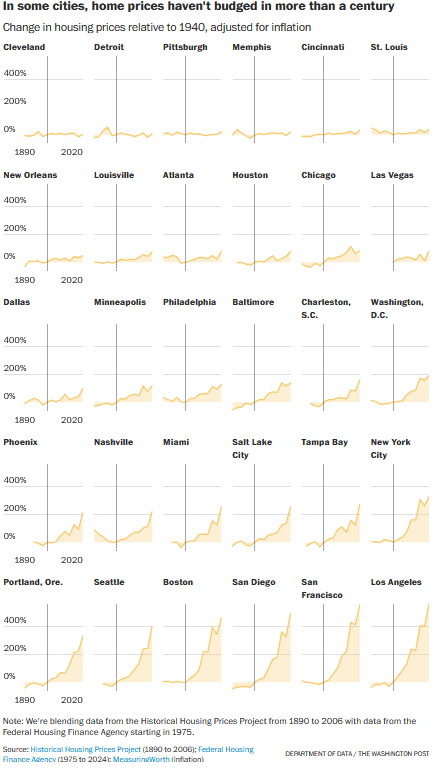

When we stopped to think about that, we couldn’t get it out of our heads. So many of us have internalized the lesson that homes are speculative, flippable investment vehicles, yet in much of the country — Cleveland, Memphis, Detroit, we could keep going — housing has been a truly quotidian commodity. There, home prices simply keep pace with inflation over the long run, no different from spaghetti or sprockets…

Consider that Dallas, Houston, Seattle and Portland, Oregon, all had what the researchers would classify as high demand for housing. But prices in Dallas and Houston have only roughly doubled in price since 1890, compared with a more than sixfold jump in Portland, or almost fivefold in Seattle…

“If prices go up,” Lyons asked us rhetorically, “does supply come on stream to follow? Do people look to build homes?”

Since 1970, the metros where housing stock grew the least relative to population growth — think Los Angeles, San Francisco, San Diego or Seattle — saw the some of the fastest home price growth. While metros that built enough housing — such as Atlanta, Phoenix and Charleston, South Carolina, saw home prices rise much less rapidly, even as their populations soared.

Does this suggest that Americans have come to view houses as investments when some places in the country have not experienced large increases in housing values over time?

For the cities with big increases over time, how do local leaders and residents see the jump in property values? It clearly leads to issues with affordable housing: rising housing values prices some people out of the market, particularly compared to what that market was and what residents had previously experienced. But rising housing costs can be viewed positively: people can sell their properties for more money and rising values can be associated with success.

This might be another reason why it is difficult to address housing issues at a national level. Housing is a very local issue and the cities in the top row of the graphic above have very different conditions compared to the cities in the bottom row.