A recent projection looked at how much American homes will be worth in a few decades:

The median U.S. home price will likely hit $1 million around the year 2050, when the millennial generation is hitting the traditional age of retirement, a top housing economist has predicted.

“Essentially, in about 25 years the national median home price will be a million dollars,” Lawrence Yun, chief economist at the National Association of Realtors®, said at a conference in Washington, DC, on Tuesday. “It may be hard to envision that, but back in 1990, the national median price was $90,000.”…

Last month, the national median sales price for existing homes was nearly $430,000. Yun used multiple scenarios to project home prices out into the future, and says each scenario pointed to roughly the same timeline to hit $1 million: about 25 years.

This makes sense over time as inflation continues. Compared to the past, houses and many other goods are more expensive.

But three factors might make this hard to swallow for a number of people:

- How much will incomes and wages keep up with the price increase of houses? Will housing be further out of reach by 2050? A million dollar price for a home will be easier for people to understand if pay keeps up with those values.

- There will be people in housing who remember the lower prices of the past and a good number who will benefit from them. Those who owned homes in 2026 will recall the median at $430k and wonder – and enjoy, if selling – the new median of $1 million. Just as those who lived in the early Levittowns saw their homes increase in value over the decades, so will those who bought homes in the early 2000s.

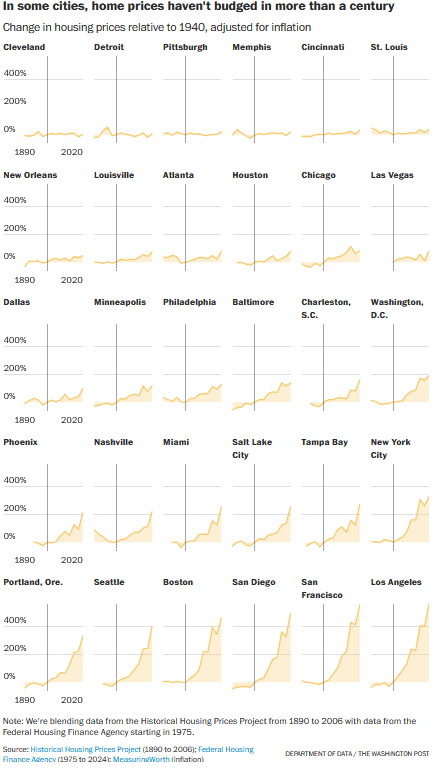

- Some places will have much higher median home values in 2050 compared to others. While this is true today, that gap may grow and highlight differences between metropolitan regions.

I wonder if the biggest consequence of this continued rise in home values will be that houses in the United States will be regarded first and foremost as investments. If the median value can double in 25 years just by owning it, this can shape who owns homes and how they treat them.