Relatively few homes are available for purchase in the United States:

Sales of existing homes rose a steeper-than-expected 3.5% in December compared with January, according to the National Association of Realtors.

Demand is surging because mortgage rates are about a full percentage point lower than they were a year ago, and the largest generation, millennials, are aging into their homebuying years.

That demand has pushed the supply of homes for sale down 8.5% annually to the lowest level since the Realtors began tracking inventory in 1982…

Sales of homes priced below $100,000 were down 7.7% annually in December, while every other price category saw increased sales. That is because there is so few for sale at the entry level. Investors have been very active in this category, turning these homes into lucrative rentals.

The article cites multiple factors at work: low mortgage rates, older millennials looking to purchase properties, and a decreased supply of cheaper homes (in part because of investors looking for rental properties).

I am curious about two things the article does not mention:

1. Who are all the actors involved in these trends? Mortgage rates are down – because federal interest rates are low? How are lenders reacting to this? Millennial homebuying might be up – what do the trends look like for other groups (particularly since homeownership is not necessarily high)? How are policymakers reacting to this shortage, particularly when affordable housing is a major concern in many markets?

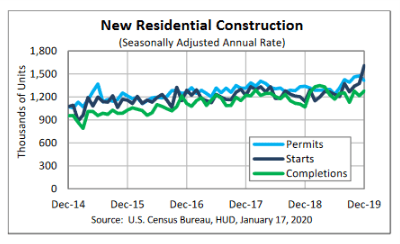

2. This seems like an opportunity for builders and developers: the supply is low, people want homes. How are builders responding? According to the Census, new housing construction is trending up in the last few years:

These converging actions and trends bear watching in a country devoted, at least in ideology, to homeownership.