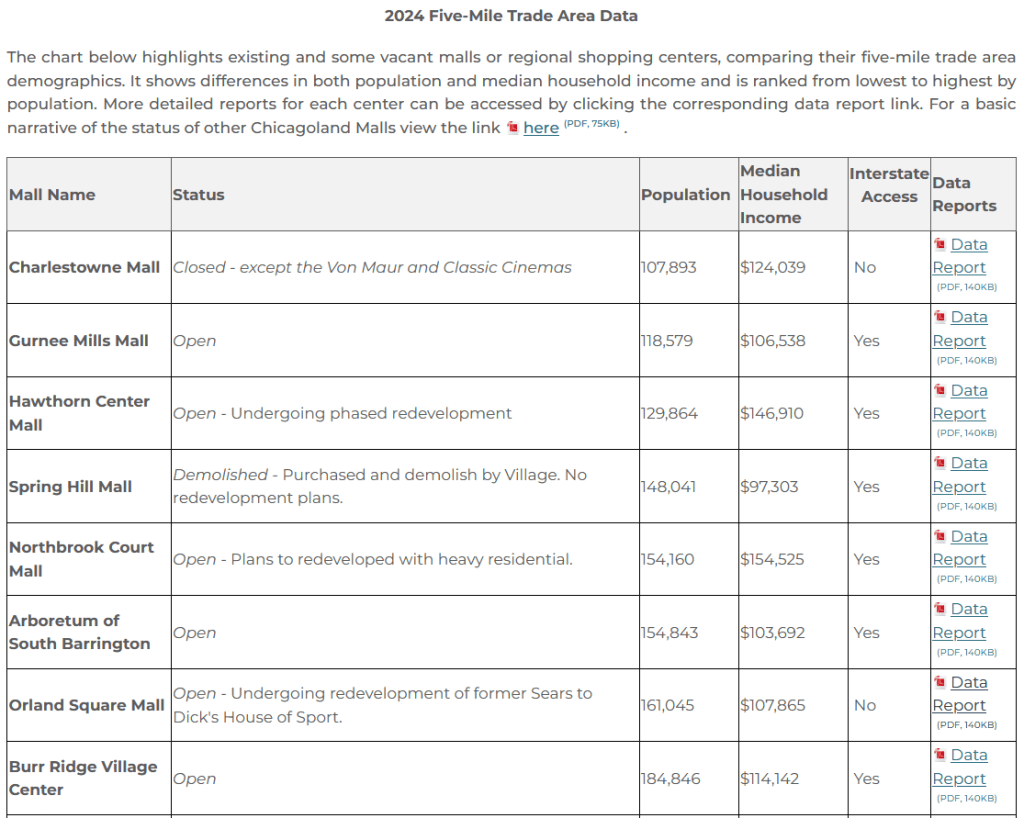

Commercial businesses such as retail stores, restaurants, and entertainment venues depend on a strong local population to generate steady sales and foot traffic. The more households that surround a shopping center, the greater the built-in customer base to support those businesses and the more attractive the redevelopment is for a developer. For Charlestowne Mall, the surrounding area has relatively low population density compared to other successful shopping corridors in the region. With fewer nearby residents, there is less day-to-day demand to sustain large-scale retail, making it harder to attract and retain major tenants. The graphic below provides the basic demographic and market data within a five-mile radius of the Charlestowne Mall site. Developers and businesses rely on this data to evaluate the market feasibility of proposed commercial uses and to understand the strength of the local customer base.

From this analysis (which continues for about 10 more malls in addition to the chart above), several features of Charlestowne stand out: the nearby population is relatively small and the mall has no interstate access. It does have a higher median household income than some malls, including the two others on the list that were demolished (but had more residents nearby with one having interstate access and another not).

So is the real story about this property about mall overdevelopment? As the number of shopping malls expanded in the growing suburbs of the end of the twentieth century, how many were doomed from the beginning? Or perhaps developers and communities were too optimistic about how many people malls might draw or projected more nearby residents than ended up living nearby. Did anyone foresee the rise of online shopping or the shifts in consumption habits?

The trend in recent years is to try to save malls with new features that will continue to pull people to the property. But the malls that are already closed – such as Charlestowne – can struggle to replace them with something local residents and leaders want. This property still has fewer people nearby and no interstate. Even if the mall building is closed, it is hard to lose the dream of the mall and all that went with it including local revenue and a local gathering spot.

Thinking about two suburban shopping malls recently demolished in the western suburbs of Chicago (here and here), how might a suburb go about marking – if at all – where the shopping mall once stood?

Both malls operated for over four decades. People from the suburb in which they were located and nearby suburbs shopped and gathered there. The communities in which they were located gathered and used the tax revenue generated by the mall.

As redevelopment plans get underway, is it worth marking where the mall once stood? Imagine a roadside marker that says “Former site of the Stratford Square Mall.” Or within the new development some indication on the ground of the footprint of the mall. Or naming some part of the new development after the mall that was once there.

Perhaps marking the former mall site in some way is going too far. Plenty of suburban redevelopment happens without much concern with what was there before. Historic preservation groups and efforts can save or identify properties worth holding on to. But it takes money and local will to remember past land uses and buildings. Would there be enough interest in remembering these shopping malls?

One feature I like about Google Streetview is that with over a decade of streetscape images, you can go back and see what an address looked like years ago. This might be possible to do with other mediums, such as overlaying older photographs or drawings over current images, but it can be difficult to track down such images. The malls will live on in Streetview, even as the sites are transformed.

So: When was the last time you were on a sound stage for a film or TV series? Even if you work in production, the answer is likely “not lately.” One well-known director recently told me that the last time they worked on the 15-stage Fox lot, their production was the only one active that day. And FilmLA’s recent sound stage report was bleak: Average stage occupancy plunged to 63 percent in 2024, down six points even from a strike-ridden 2023.

Compare that to 2016, when stages hummed along at 96 percent occupancy level, or the we-all-agree-it-was-a-bubble Peak TV year of 2022 when levels bounced back up to 90 percent during the post-pandemic recovery. Investors from Blackstone to TPG have stakes in sound stage properties, so it’s not just Hollywood worried about production. Just days ago, sound stage titan Hudson Pacific Properties — the Blackstone-backed owner of Sunset Bronson Studios, which is leased to Netflix — got hit with a credit rating cut. S&P Global called out the company’s “weakened studio business performance” and declining leased studio space, which dipped to 73.8 percent from 76.9 percent the year prior…

On a macro level, sound stages are in trouble — a reflection of the times. Production continues to be offshored to states and countries with more appealing tax incentives and cost structures, the correction from Peak TV means fewer series are being made, and the post-strike job market is still sluggish. While Gov. Gavin Newsom and others are pushing for a big new California tax credit plus other legislative moves to make filming here more accessible (#StayinLA), the industry is still reeling from a few years of blows, and some entertainment workers have left L.A. behind.

While the empty sound stages may be the result of specific issues in the TV and film industry, the comparison to shopping malls is particular interesting. Do we now just assume shopping malls are past their peak? That many of them are dead? That they are the exemplar of buildings that were once thriving but are empty now?

Vacant buildings are a problem for a number of industries and communities (see examples here and here). Empty buildings mean less work or activity is taking place. Empty buildings can lead to perception issues and ne’er-do-wells possibly causing problems. Empty buildings could lead to reduced tax revenues.

If shopping malls are the best comparison for these particular empty buildings, one lesson we might take: it will take years to figure out what to do with these properties. Will activity pick up in production again? Could there be temporary uses for these structures? If redevelopment is pursued by developers, do neighbors and communities want what might be there next?

Dead shopping malls could turn into zombie shopping malls: ones that slightly change form but stick around for years with limited activity and change. Whether sound stages follow a similar path remains to be seen.

From 1959 through the early 1980s, more than two hundred American cities closed blocks of their downtowns to car traffic. B 2000, fewer than twenty-four of those original malls remained. (89-90)

As people and shopping moved to the suburbs, larger cities responded by trying to create something like an outdoor mall on busy urban shopping streets. But the experiment did not work:

By 2000, fewer than twenty-four of these original malls remained. The design intervention that was supposed to bring people back from the suburban mall had, instead, exacerbated the very problem it was trying to solve, turning downtown into car-centric, retail-first monocultures rather than pedestrian-first, mixed-use places. (90)

Many cities thought this was the answer but it turned out not to be; few of the pedestrian malls survived even a few decades.

Two thoughts hearing this account:

Cities did not know what to do regarding the millions of Americans who moved out of big cities and to the suburbs after World War Two. Were they moving out of cities in part because of shopping opportunities? This was not the biggest issue but cities hoped they could at least attract more visitors with pedestrian malls.

The copycat nature of retail development across places is interesting to consider. As malls proliferated, often borrowing architecture and techniques regardless of location, many communities also jumped on the pedestrian mall bandwagon. And then when they did not bring about the desired changes, they disappeared en masse as well. It makes sense that cities and developers would look to each other to see what works but it also seems like it can lead to fads and trying to shoehorn generic solutions to what can be complex local settings.

When JonasCon, an all-day special event celebrating the 20 years since the debut of the hit boy band the Jonas Brothers, was first announced in mid-February, anyone who still cared about the JoBros (myself included) thought it would be a disaster. After all, the announcement came less than two months before the event; information about what was actually going to happen during the convention was nowhere to be found, even mere weeks away; and it didn’t help matters that there were last-minute reports that the Jonas Brothers were struggling to find sponsors for what would likely be a “complete and chaotic mess.” Hints of an impending trainwreck angered fans; not only were they financially invested in traveling to the event, but they were also feeling protective over (and worried about) the reputation of the once-popular band of brothers, who have been left behind in an era short on boy bands and heavy on “popgirlies.”

But what actually happened on that Sunday in March, at the behemoth that is the American Dream mall in East Rutherford, New Jersey, wasn’t the reincarnation of Fyre Fest that everyone was expecting. It was something else entirely…

Being inside of the bubble of the teenage dream—while literally ensconced in the American Dream—makes you forget that the real world is still happening.

Four things seem to be converging here that add up to the American Dream:

A shopping mall/attraction site that calls itself American Dream. The large thriving shopping mall is a great embodiment of the postwar suburban American Dream. (In terms of spaces, it might only trail the single-family home and yard as the epitome of the American Dream for a certain era.

The teenager experience is a unique one in American society. The mix of independence and growing up and testing out adult things can come together into a heady time where experiences and patterns can prove influential for the rest of life.

Music gets wrapped up in #2 as an important narrative element. Certain artists or genres can speak to teenagers in ways they might not to adults The music and the memories that go along with the music are powerful.

The American Dream is not just an idea; it can be experienced. The setting here is a fan convention that brings together in a suburban setting people who enjoy particular music. They get to enjoy the music, the energy, and meeting people at one time. There are other experiences that can be the American Dream – perhaps a backyard cookout, perhaps driving fast down a road – but the fans at this event seem to get to experience something that helps them ignore what else may be happening.

Paramus officials say they’re exploring a lawsuit against American Dream, after learning that retail shops at the Meadowlands megamall are open for business on Sundays in defiance of Bergen County’s Blue Laws.

The stores at American Dream have been operating in violation of those laws for nearly a year, The Record and NorthJersey.com reported last week, despite the county’s longstanding prohibitions against the sale of nonessential items such as furniture, appliances and clothing. The restrictions, in place since the 17th century, exempt some services, including groceries and drugstores.

Paramus residents in particular have been proponents of the Blue Laws over the years. Supporters say they grant them a day of reprieve from heavy traffic that plagues the town the rest of the week due to the borough’s four malls…

“Being mayor of Paramus, I know how important the Blue Laws are to our way of life and the peacefulness of Sundays,” he said in an interview. “[It gives us] the ability to move around town, the ability for our emergency services to have less calls and regroup. As mayor, I’m going to fight like heck for Paramus and the county as a whole.”

Such regulations used to be more common across the United States. It can be surprising for some to hear that places would continue to follow these guidelines or businesses might choose to follow them (see some of the conversations around Chik-Fil-A in different parts of the country regarding their practice of not being open on Sundays). Even the article above notes that these restrictions date back hundreds of years; are these simply archaic local idiosyncrasies?

The explanations given by these suburbanites regarding the purposes of the blue laws are interesting in today’s context. Is Sunday a day of rest from traffic? Are the malls bringing in so many vehicles from outside the county that their closure on one day makes it easier for locals to get around? Do the EMTs and police need time on Sunday to regroup from all of the accidents and calls on the other six days of the week? The website of another suburb in the county highlights the Sunday prohibitions but does not say why they exist.

My guess is that the Bergen blue laws originate in religious motivations. Sunday is the Christian day of rest. I wonder how much of the current support for the blue laws is religious support as opposed for other reasons for having a day of rest.

Many municipalities in the United States want more local revenue. Having multiple local shopping malls is a good thing because it can increase commercial activity and sales tax revenues. Can communities still thrive if they limit shopping mall activity on one of the weekend days?

While the suburbs are known first for their emphasis on single-family homes, they are also full of commercial activity. Specifically, shopping malls, retailers, and strip malls dot the suburban landscape. Drive down major roadways through the American suburbs and you are likely to see retail activity all over the place.

With the ongoing shift toward online shopping and shopping by delivery, what happens to all of these locations? The shopping mall has been suffering for years. A quintessential suburban feature with acres of free parking, numerous retailers in one location, and a place for teenagers and others to hang out, many malls will not survive. Similarly, big box stores and smaller retailers are also closing.

Suburban communities have been working on this for years. Can the shopping mall become more of an entertainment and restaurant center? Can it survive with apartments and housing added on site? Can they be demolished, rezoned, and be home to thriving new developments? For the big box store, what can fill that space?

In all of these plans and activity, there are some common patterns at work:

Suburbs want to replace the revenue malls and retailers produced. This can mean they hold on to ideas of retail or revenue producing uses for a long time.

What replaces the retail locations should not significantly drain local services.

Redevelopment, even if local actors generally agree on what should be done, can take a while. Some of these malls and retail locations have been there for decades. Their particular location and context may vary but changes can affect local character and experiences.

At the same time, some suburban communities will continue to have thriving malls and retail locations. Will this only be in wealthier communities or in ones with advantageous locations within a region or among ones that provide certain desirable amenities? Even if the number of shopping malls, strip malls, and big box stores declines this year, they are not going away completely anytime soon. But the patterns of where there are may continue to fuel differences between suburbs in regions.

A crop of new restaurants and a Dave & Buster’s have been added to the mix. A grocery store is slated to open next year. In the clearest sign of the mall’s resurgence, a developer has kicked off the first phase of a luxury apartment project called “Yorktown Reserve.”

The old Carson’s department store will be dismantled to pave the way for public green space between the mall and the apartments. Inward-facing mall spaces will be turned outward. Facing the park will be a new, two-story entrance directly into the center of the mall.

What does “Reserve” refer to? The first thought that came to mind: wine. Quoting a possible definition of reserve in the Merriam-Webster Dictionary:

9: a wine made from select grapes, bottled on the maker’s premises, and aged differently from the maker’s other wines of the same vintage

Upon further thought, this does not strike me as the meaning. Apartments tasting like a fine wine? How about a different definition of reserve:

1: something reserved or set aside for a particular purpose, use, or reason: such as…

b: a tract (as of public land) set apart : reservation

A reserve as in a set apart piece of land? This seems more like the meaning with the apartments next to a new “public green space” and the mall.

Once the apartments are constructed, I would be interested to hear residents and neighbors reflect on this name. Does it feel like a reserve? Does the name imply a certain price point and residential experience?

Golf Mill Shopping Center opened in 1960 as an open-air mall. Later, it was enclosed, and the iconic Mill Run Playhouse was built on the grounds. The theater, before it closed in 1984, hosted acts such as Chicago native Shecky Greene and Frank Sinatra.

Today, the mall has more than 1 million square feet of leasable space in addition to a nine-story office tower. Target and JCPenney are two of its biggest anchors, alongside AMC Theatres, Ulta, Burlington and Ross…

Alpogianis and other city officials see the future of the 80-acre site as “live, work, play” — an increasingly popular phrase for mixed-use developments that have virtually everything a resident could need on site. The Golf Mill Shopping Center redevelopment — to be called Golf Mill Town Center — will aim to be one of Niles’ premier destinations in the absence of a traditional downtown.

The first phase of redevelopment will include an overhaul of the mall’s retail, along with new luxury apartments and restaurants, Alpogianis said.

He said the project will be 70% retail and entertainment and 30% residential and other uses — the latter of which includes the “very good” possibility of a hotel and office, depending on market conditions.

The shopping mall redevelopment described here is common these days: add housing, restaurants, and different retail options to what was a mall with declining activity and revenue. The goal is more of a 24 hour a day place where a combination of residential, commercial, and recreational activity makes it more like a lively neighborhood.

What struck me here was the idea that such a redevelopment could help address a different issue in the suburb: no traditional downtown. In the Chicago area, such a downtown would typically be located along a railroad line connecting suburbs to downtown. Niles is more of in-between two railroad lines and the community had a small population until a population explosion in the 1950s (over 400% growth).

While the shopping mall is often viewed as a postwar substitute for public space, could all of these mall redevelopments lead to new suburban downtowns? The mixed-use developments are often intended to be more walkable, at least to the new residents who live there, and provide social spaces. Whether this actually happens is another matter; will the redeveloped malls be connected to a larger walkable grid in suburbia? Will people still need to drive to the redevelopment? Once people are living on site, how many will regularly make use of the nearby amenities as opposed to driving elsewhere?

The shopping mall may come and go in many suburbs but the quest for something like a downtown may continue.

The Skokie Village Board gave tentative approval at its Oct. 8 meeting for developers to build hundreds of luxury apartments across three buildings at the upscale Westfield Old Orchard Shopping Center.

The first phase of construction would create 425 apartments between two mixed-use buildings, one five stories tall and one seven stories tall. The second construction phase would be for an additional seven-story building that could be used for more apartments or a hotel, said Stephen Fluhr, Unibail-Rodamco-Westfield’s senior vice president of development…

The additions to the mall were met with criticism by an affordable housing group, which blasted the Village Board for approving plans they saw as having too few affordable apartments.

The first phase would put two buildings in the area of the former Bloomingdale’s retail space in the northwest part of the mall, south of Old Orchard Road and east of Lavergne Avenue. The developers’ intention is to create a new neighborhood complete with parks, restaurants and spaces for concerts and farmers markets, according to Fluhr. The development is a partnership with the mall’s owner URW and Focus, a development group that is also in the process of building apartments near malls in Vernon Hills and Aurora.

Many malls would like to add housing to their property (examples from the Chicago suburbs to southern California): it makes use of vacant shopping space and provides local residents who might visit stores, restaurants, and entertainment options at the mall.

But, as communities consider affordable housing, why not include affordable housing as part of redeveloped housing at the mall? Many suburbs have limited greenfield development options so redevelopment provides an opportunity for affordable housing. Or affordable housing could provide housing for people working at the mall or working near the mall as shopping malls tend to be close to all sorts of businesses and jobs.

The bigger issue at hand is likely this: how many suburbs are truly willing to add affordable housing? And if they say they want to add such housing or have local regulations that require it, where will they allow it be located?