“We have a supply problem with housing,” Marc Norman, associate dean at the NYU Schack Institute of Real Estate, told Yahoo Finance Live (video above). “We’ll see the price declines, but I think the income gains that we are seeing lately are still not keeping up with the prices that we are seeing in the market — in most markets.”…

“We, for the last 20 years, have underbuilt the housing,” Norman said. “In 2008, we saw the sort of demand go down, but it never came back in terms of supply.”

After the 2008 real estate crash, residential construction activities in the private sector never recovered to the level of 2006. Although home building slowly increased year over year during the last decade, projects remained well below early 2000 levels, according to figures from the Census Bureau and. Department of Housing and Urban Development.

Several thoughts in response:

The United States has never fully recovered from the housing bubble in the late 2000s. The rise in housing values, homeownership, and lending activity led to a lot of trouble.

How much money has the real estate and development sector made since the late 2000s? How much money has been left on the table by not building (or not being able to build, as discussed in the article, due to zoning and other restrictions)?

How many older homes are retrofitted or renovated to meet current standards and tastes each year compared to how many new housing units are needed? Both routes could help provide housing.

American households lost about $6.8 trillion in wealth over the first three quarters of 2022 as the stock market shed more than 25% of its value, the Federal Reserve reported Friday in the government’s quarterly financial accounts.

Nominal net worth fell 4.6% to $143.3 trillion, as the market value of assets fell by $6 trillion and liabilities rose by about $900 billion. Households’ balance sheets were propped up by a 10% increase in home equity, which is the greatest source of wealth for most American families…

Homeowners, in particular, were in good shape financially as September ended, with the equity in their houses rising to a near-record 70.5% of market value from a record low of 46% in 2012. But if home prices continue to fall as they have done in the past several months, homeowners without much exposure to the stock market will begin to feel poorer. What will happen to home prices as mortgage rates rise is a major unknown facing policy makers and homeowners alike.

Thinking out loud: after what happened in the late 2000s with housing prices, how would people respond to a significant reduction in housing values? Or, how would this be received if inflation is ongoing and the stock market struggles? For now, some can rest assured that their homes will retain value. But, this is not guaranteed.

Thinking more about yesterday’s post on cooling home values in certain housing markets, how many people benefit from the lower prices? The typical emphasis in such economic times is to note the difficulty of buying a home when interest rates are higher and there is economic uncertainty.

But, lower prices means some might be able to buy when they could not otherwise. The hottest markets in good economic times have high prices and lots of competition. Even as borrowing money is harder in a recession, prices can be lower and the competition might not be as stiff.

Some people are still buying and selling homes during economic downturns. This leads to a long-term question: are those who buy during a recession more or less likely to hold tightly to the idea of a home as an investment? Is buying at the height of the market – famously, such as right before the housing bubble burst in the late 2000s – tied to a deeper focus on property values and a strong return on investment? Or, because a home purchased during a recession might emphasize scarcity and economic uncertainty, might this lead to more concerns about property values?

With houses selling for so much, you’d think there would be a big incentive for developers to throw up new units, which they can do quite quickly. I still remember driving around New Jersey during the McMansion boom and being amazed at how quickly houses went up. Why aren’t the developers rushing in now?

In correspondence, my old M.I.T. classmate and economist Charles Steindel pointed me to the likely answer: It’s the supply chain, stupid.

This makes sense given current conditions: an increased cost in materials plus difficulty acquiring materials might translate into fewer profits in building McMansions.

I do wonder if there are additional factors at work. A few quick ideas:

McMansions have an established reputation. There are still plenty of people who will buy one but there is also a clear connotation about the home when this specific term is used. Hence, “luxury homes” instead.

There is more money to be made in even larger houses. Why build McMansions when there are enough customers for even larger and/or more opulent homes? Perhaps the money in McMansions comes at a sizable building scale while the per lot/house profits on even more expensive homes is preferred.

McMansions are not going away as they are an established part of the American housing stock. But, it will be worth watching how many new ones are constructed, where, and by whom.

Speaking at a Arizona high school in August 2013, President Obama both addressed specific policies he hoped Congress would pass regarding homeownership as well as the dream of middle-class homeownership. Here is part of the speech connecting middle-class aspirations and homeownership:

What we want to do is put forward ideas that will help millions of responsible, middle-class homeowners who still need relief. And we want to help hardworking Americans who dream of owning their own home fair and square, have a down payment, are willing to make those payments, understand that owning a home requires responsibility. And there are some immediate actions we could take right now that would help on that front, that would make a difference. So let me just list a couple of them…

So I want to be honest with you. No program or policy is going to solve all the problems in a multi-trillion dollar housing market. The housing bubble went up so high, the heights it reached before it burst were so unsustainable, that we knew it was going to take some time for us to fully recover. But if we take the steps that I talked about today, then I know we will restore not just our home values, but also our common values. We’ll make owning a home a symbol of responsibility, not speculation — a source of security for generations to come, just like it was for my grandparents. I want it to be just like that for all the young people who are here today and their children and their grandchildren. (Applause.)

These sections echo common themes of how the American public often thinks about housing:

Homeownership is a symbol of successful hard work and responsibility. Put it in the time and effort and it should lead to a home.

Systems and particular actors can conspire against possible homeowners – financial speculators, irresponsible people – but the government should be in the business of helping people achieve homeownership.

Homeownership is a goal across American generations, from grandparents to current adults to future children.

The middle class and homeownership are intertwined.

Even as President Obama sought specific actions, he appealed to cultural goals and narratives very familiar in American life.

Rampant speculation and skyrocketing property values have left Kelman feeling almost nostalgic for those years leading up to 2008, which, in retrospect, were the last time the working poor could reasonably aspire to home ownership in America. “I used to read stories about strawberry pickers buying McMansions in central California, and everybody viewed that as just the absolute apex of insanity,” Kelman told me. “But reading Piketty five years later, is it so bad that the strawberry picker had a nice house?”

Conceding that the picker probably could not afford his McMansion, and that the loans that put him in it were untenable, Kelman nevertheless liked this gaudy permutation of the American Dream. More than that, he disliked the level of “elitist judgment” surrounding these types of homes, which he views as nothing more sinister than the market’s attempt to grapple with problems politicians are content to ignore. In Kelman’s view, the left is eager to help the poor rent homes but not own them, while the right tends to ignore their plight altogether. Meanwhile, rampant NIMBYism prevents the kind of building that might help bring home prices back down to earth.

It had put him in a mood to reflect somewhat darkly on the future of housing in America. “The original premise of my stint at Redfin was that we’re selling the American Dream and the idea that everyone can afford a house sooner or later if they work hard and play by the rules,” he said. “Recently, I’ve had this feeling that there are so many people who are never going to become Redfin customers — that maybe the product we’ve been selling just isn’t a middle-class product anymore but an affluent product.” In February, anticipating a future in which homeownership is out of reach for more and more people, Redfin spent $608 million to acquire RentPath and its portfolio of apartment-leasing sites.

The story as written suggests that Kelman originally subscribed to the idea that Americans who work hard and follow the rules would be able to purchase a home. This has been at least an implicit idea for decades, particularly in the postwar era. He did not like commentary that suggested some were less deserving to own homes or political positions that limited homeownership. But, after the housing bubble burst in the late 2000s, he realized homeownership was not available to all.

If this is correct, the Redfin pivot to apartment-leasing is an interesting choice. This could be a good business decision as rental housing is needed in many communities. At the same time, this does not necessarily line what up with what Kelman expressed. Apartments can provide housing but they do not provide the same kinds of opportunities as housing – such as building wealth – nor are apartment dwellers viewed the same way as homeowners. Americans continue to say that they would prefer to own a home.

Redfin and similar sites could play important roles in what homeownership looks like in the future. Exactly what influence they will have is less clear.

For millennials, many of whom are getting married later in life, swimming in student-loan debt and facing soaring home prices, homeownership can feel more like a fantasy than an achievable goal. So, some first-time home buyers are taking a more creative route to make it happen—by pooling their finances with partners, friends or roommates.

Since 2014, when millennials became the largest share of home buyers in the U.S., the number of home and condo sales across the country by co-buyers has soared. The number of co-buyers with different last names increased by 771% between 2014 and 2021, according to data from real-estate analytics firm Attom Data Solution.

The pandemic added fuel to that trend, according to data from the National Association of Realtors. Among all age groups during the early pandemic months—April to June 2020—11% of buyers purchased as an unmarried couple and 3% as “other” (essentially, roommates). Those numbers were up from 9% and 2%, respectively, in the previous year.

This is an interesting situation: Americans continue to want to purchase homes. However, this is not within the reach of many unless they have ways to draw on additional resources.

I have heard many warnings over the years about co-signing loans, even among family. Some of these arrangements could present complications in the long run:

Legal experts advise buyers to consult a real-estate attorney to help write a co-ownership agreement that covers every possible scenario, from job loss to marriage to personal fallouts. For example, who will hire the handyman if there is a plumbing issue? Who is in charge of collecting and making the mortgage payments? If one co-owner moves away, will the other co-owners have an option to buy them out or will there be a forced sale of the home?

While this is still a small minority of homeowners, it is worth paying attention to with high housing prices and economic anxiety.

Today, if you’re looking for one, you’re likely to see only about half as many homes for sale as were available last winter, according to data from Altos Research, a firm that tracks the market nationwide. That’s a record-shattering decline in inventory, following years of steady erosion…

There are lots of steps along the “property ladder,” as Professor Keys put it, that are hard to imagine people taking mid-pandemic: Who would move into an assisted living facility or nursing home right now (freeing up a longtime family home)? Who would commit to a “forever home” (freeing up their starter house) when it’s unclear what remote work will look like in six months?…

For more than a decade, less housing has been built relative to historical averages. The housing crash decimated the home building industry and pushed many construction workers into other jobs. Local building restrictions and neighbor objections have slowed new construction. President Trump’s strict immigration policies further restricted the labor supply in the industry, and his tariffs pushed up the price of building materials…

Right now, in a number of metro areas, home prices and rents aren’t just drifting apart; they’re moving in opposite directions. Prices are rising while rents are falling.

The article ends on a note of uncertainty: where might the housing market go from here? But, I wonder if it is worth digging more into the past to think about how we got here. Several things come to mind:

COVID-19 is a very unique situation. As the article notes, this seems to have affected rental and home prices in different ways as suddenly people were interested in homes in particular areas and not so interested in rental properties in other areas. Figuring out the long-term effects of this will take time; will people return back to work in big offices, whether in the city or suburban office parks? Is this a significant change or will markets return back to earlier patterns with more time removed from COVID-19?

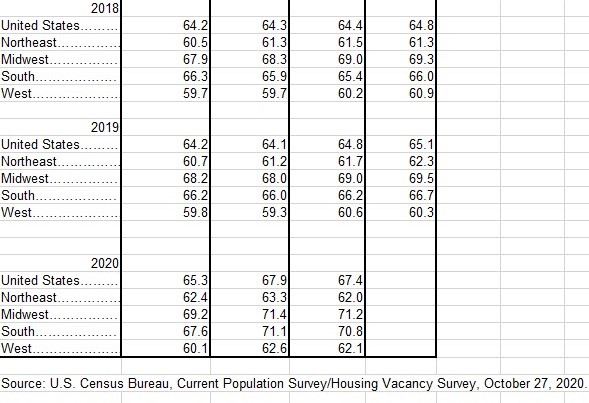

During 2020, the homeownership rate jumped to roughly 67%, up nearly 3% from a year earlier after remaining largely flat for a decade, according to the Census Bureau.

The article attributes this jump to COVID-19 and the shift of people from cities to suburbs.

If indeed homeownership jumped nearly three percentage points in one year, this is a big shift. In the historical data table from the Census (Table 14), it is rare to find huge jumps year to year. The fallout from the late 2000s happened in relatively small decreases.

A big jump in 2020 has implications for multiple actors: communities with new residents and others losing residents; those involved in the housing industry from develoeprs to realtors to investors to landlords; residents as those with resources took advantage of purchasing opportunities while others struggled to hold on and payments are looming.

How will these dueling pressures – buying homes amid COVID-19 and low mortgage rates at the same time as economic uncertainty – play out?

“When suburbanites come intown, they want to bring the suburbs with them. The day of the urban pioneer is gone,” says attorney Lee Meadows. The heart-pine floors, plaster walls, and black-and-white tile bathrooms of compact 1920s Craftsman bungalows can’t compete with the wired-for-plasma-TV mantel and Carrera marble–accented master bath of that “Neo-Craftsman” on Oakdale. (August 2007)

This is a short description but this seems to capture the McMansion era well:

-Bringing particular expectations about homes to cities and suburbs, whether they fit or not.

-Preferring new larger homes with features over historic homes.

-Particular features of these new homes included flat screens mounted over the mantel, marble in the bathrooms, and aping established architectural styles.

All that might be missing is the spread of McMansions in Sunbelt regions and the size of these homes, especially on certain smaller lots.

Of course, this comes before the housing bubble burst and more hardened opposition to McMansions. These homes are still constructed today in cities and suburbs but the thrill of McMansions has diminished. In other words, the “irrational exuberance” of McMansions is gone except perhaps in particular locations and for certain builders and buyers. For this reason, and perhaps many others, 2007 seems very far away.