Not everyone agrees Zillow is good. Like Uber, the company has weathered a barrage of industry resistance, naysayers and litigation in its conquest. But its dominance is unquestionable. Arizona’s Kris Mayes, one of five state attorneys general suing Zillow over alleged anticompetitive practices, has called it “a gorilla-sized company.” In 2024, Zillow reported annual revenue of $2.2 billion; analysts estimate it will be even higher in 2025 and 2026.

People associate Zillow with homebuyers, but it actually makes around 70% of its revenue from agents, who pay the company for customer leads. Wacksman thinks a lot about how to keep the agents happy (hence tonight’s Musgraves concert). He knows many of them have reason to loathe Zillow, which has empowered consumers with market data and property history previously known only to licensed agents. Many of these “information arbiters,” as Wacksman describes pre-internet agents, were ruined during Zillow’s rise. “Our original mission statement was ‘power to the people,’ because it was about giving the nonprofessional access to data that only the professionals had,” he says. “It obviously worked.”

So Zillow opened up possibilities for potential homebuyers but then makes its money by providing their information back to the people who used to exclusively have this information? I am trying to think how this might work in other industries. Car listing sites that then provide leads to dealers looking for buyers or sellers? Ride sharing companies selling info to taxis for riders? Online marketplace sites selling user info to sellers?

If anything, this is a reminder of one of the revenue drivers of the online/social media world: data and information about users. Websites and platforms have information about users. What they see and linger on. What they engage with. Personal information they offer as part of accounts and profiles. How they interact with other actors. This is valuable for companies and organizations who have products or services to offer.

At the same time, is this revenue model similar to how other real estate websites operate? Does realtor.com make money off customer leads? Or Redfin? Are there other ways to make money off real estate listings available to a broad audience?

A real estate agent might know a lot about neighborhoods or communities. Looking at the local marketing realtors do, I see that they claim to know about different suburbs. In particular, they have knowledge about the local housing market through what has sold and what has not. They can also talk about other aspects of the community, such as schools and nearby amenities.

If I go to websites like Zillow or Realtors.com, they offer neighborhood information with each property listing. This includes a map, walkability scores, ratings of local schools, other nearby listings and recent sales, and more.

But what does it take to know about a neighborhood? Who can accurately describe what it is like to live there or how the character of a place plays out? Does anyone offer insights from local residents? Do real estate agents live in the communities they sell in or have secondhand information from local residents and organizations?

This reminds me of two posts I put together years ago on how to learn about a suburb. There are lots of sources of information about communities and some of it is available online. But some of it is not. Talking to people or walking through a community or reading local histories can provide some insights that are harder to intuit online.

Who else might be a “neighborhood savant”? A local journalist, where they are still available. A local political official or a longstanding member of a community institution. A local historian. Residents who take an interest in and actively participate in their neighborhood.

So, when the National Association of Realtors recently adopted a policy allowing limited off-MLS marketing, Zillow announced it would permanently ban any listing not posted to the MLS within one day. Essentially, Zillow — a company that doesn’t sell homes — is asserting it gets to decide how you can market and sell your home.

Zillow claims it is protecting consumers from off-MLS marketing, which it says leads to longer market times and lower prices. But a 2024 study by Midwest Real Estate Data — the MLS serving Chicagoland — shows the exact opposite. MRED offers a Private Listing Network that shares listings with all member agents without circulating them to public websites. Homes first marketed through MRED’s Private Listing Network sold 55% faster, for more money, and at a higher percentage of list price (97.5% versus 95.4%) than those listed publicly from day one.

Our own experience across tens of thousands of transactions confirms the findings of this study. At @properties Christie’s International Real Estate, we developed a “private-to-prominent” listing strategy that starts with an off-MLS marketing period and builds to a full public offering. This approach has several benefits. It allows a seller and their agent to prepare the home for sale while building interest and demand. It also gives them an opportunity to test a price without having Zillow or other websites display any reductions that might be made prior to the public listing. And the listing does not accumulate market time during this premarketing phase. (Typically, as market times increase, buyer interest decreases.)

This approach can result in faster, higher-value sales, often before the home ever hits the MLS, or Zillow. Most importantly, it keeps the seller in control. They choose when to list publicly and can accept or reject an offer at any time.

The key here is at the end: “it keeps the seller in control.” Should the seller be the one calling all the shots and having the advantages?

Another argument could be made that the seller having the primary options limits potential buyers. Is the home reaching all the possible purchasers? If it is on a private network first, how often does it reach the general public? Could private listings build off existing networks, reproducing inequalities?

Or should Zillow and other actors play the primary role as many Americans look for real estate online? Is this more of a tug-of-war between the established real estate industry and the online competitors who offer information for any searchers without the need to contact an agent? There are a lot of jobs and a lot of money at stake.

Is there any role for communities or people who might want to access certain communities down the road? If the strength of local real estate is often taken as a sign of local vibrancy and status, should this only involve private actors?

I suspect this discussion will continue as different actors look for an edge in real estate. Hopefully this does not come down to solely who can lobby the most effectively.

Just how accurate are those numbers, though? Until the house actually trades hands, it’s impossible to say. Zillow’s own explanation of the methodology, and its outcomes, can be misleading. The model, the company says, is based on thousands of data points from public sources like county records, tax documents, and multiple listing services — local databases used by real-estate agents where most homes are advertised for sale. Zillow’s formula also incorporates user-submitted info: If you get a fancy new kitchen, for example, your Zestimate might see a nice bump if you let the company know. Zillow makes sure to note that the Zestimate can’t replace an actual appraisal, but articles on its website also hail the tool as a “powerful starting point in determining a home’s value” and “generally quite accurate.” The median error rate for on-market homes is just 2.4%, per the company’s website, while the median error rate for off-market homes is 7.49%. Not bad, you might think.

But that’s where things get sticky. By definition, half of homes sell within the median error rate, e.g., within 2.4% of the Zestimate in either direction for on-market homes. But the other half don’t, and Zillow doesn’t offer many details on how bad those misses are. And while the Zestimate is appealing because it attempts to measure what a house is worth even when it’s not for sale, it becomes much more accurate when a house actually hits the market. That’s because it’s leaning on actual humans, not computers, to do a lot of the grunt work. When somebody lists their house for sale, the Zestimate will adjust to include all the new seller-provided info: new photos, details on recent renovations, and, most importantly, the list price. The Zestimate keeps adjusting until the house actually sells. At that point, the difference between the sale price and the latest Zestimate is used to calculate the on-market error rate, which, again, is pretty good: In Austin, for instance, a little more than 94% of on-market homes end up selling for within 10% of the last Zestimate before the deal goes through. But Zillow also keeps a second Zestimate humming in the background, one that never sees the light of day. This version doesn’t factor in the list price — it’s carrying on as if the house never went up for sale at all. Instead, it’s used to calculate the “off-market” error rate. When the house sells, the difference between the final price and this shadow algorithm reveals an error rate that’s much less satisfactory: In Austin, only about 66% of these “off-market Zestimates” come within 10% of the actual sale price. In Atlanta, it’s 65%; Chicago, 58%; Nashville, 63%; Seattle, 69%. At today’s median home price of $420,000, a 10% error would mean a difference of more than $40,000.

Without sellers spoonfeeding Zillow the most crucial piece of information — the list price — the Zestimate is hamstrung. It’s a lot easier to estimate what a home will sell for once the sellers broadcast, “Hey, this is the price we’re trying to sell for.” Because the vast majority of sellers work with an agent, the list price is also usually based on that agent’s knowledge of the local market, the finer details of the house, and comparable sales in the area. This September, per Zillow’s own data, the typical home sold for 99.8% of the list price — almost exactly spot on. That may not always be the case, but the list price is generally a good indicator of the sale figure down the line. For a computer model of home prices, it’s basically the prized data point. In the world of AVMs, models that achieve success by fitting their results to list prices are deemed “springy” or “bouncy” — like a ball tethered to a string, they won’t stray too far. Several people I talked to for this story say they’ve seen this in action with Zillow’s model: A seller lists a home and asks for a number significantly different from the Zestimate, and then watches as the Zestimate moves within a respectable distance of that list price anyway. Zillow itself makes no secret of the fact that it leans on the list price to arrive at its own estimate…

So the Zestimate isn’t exactly unique, and it’s far from the best. But to the average internet surfer, no AVM carries the weight, or swagger, of the original. To someone like Jonathan Miller, the president and CEO of the appraisal and consulting company Miller Samuel, the enduring appeal of the Zestimate is maddening. “When you think of the Zestimate, for many, it gives a false anchor for what the value actually is,” Miller says.

Multiple factors are at play here. Who has what information about housing and housing values? How is the value calculated? And what is the distribution of the comparison of the estimated value to the actual sales value? Some of this involves data, some involves algorithms.

It also sounds like part of the story is that Zillow has built one of the more effective brands in this space. Even if the estimates are not exactly right, people are drawn to Zillow. What would happen if competitors advertised that they are more accurate? Would this be enough to move people from using Zillow?

Given all of this, who can build the most accurate number might not be the “winner.” Is the goal to best model the housing market or is the goal to attract users? These two goals might go together but they might not.

Since he started the account in December 2020, it has exploded into a social media phenomenon, amassing more than 4 million followers across the major social media platforms and spinning off an HGTV show that debuts next month with Mezrahi as executive producer. Throughout it all, Mezrahi’s recipe has remained mostly unchanged: Find the zaniest homes on the market – castle-themed mansions with full drawbridges, for example – then blast them out to the internet with a bit of pithy commentary, and watch the clicks, likes and shares pile up. The simplicity of the premise is part of the brilliance; it’s the result of the decade-plus that Mezrahi spent charting the internet’s fascinations as social media director for BuzzFeed.

Does all this interest in houses translate into money?

None of this, however, was enough to save Mezrahi at BuzzFeed. The now-struggling company laid him off last spring. He had survived previous cuts, “but eventually you don’t last, especially as a strategist kind of person,” Mezrahi says. Already, he’d been mulling the prospect of leaving the full-time gig to focus entirely on his personal projects. BuzzFeed simply made the choice for him…

Still, there is one thing that Mezrahi shares in common with the rest of them: He’s trying to figure out how to make more money off the internet. Aside from the HGTV executive producer credit, most of Zillow Gone Wild’s revenue comes from ads. He did one for “The Bachelor,” posting what looked like a typical listing but for the show’s famed house. PopTarts and Royal Caribbean have also paid him to promote fake listings for a house made of PopTarts, and for the new Icon of the Seas cruise ship.

But the account still brings in “very little” money, he says. He imagines a future where his newsletter has a paid classified section or where he dedicates more time to growing a YouTube audience because that platform can be the most lucrative.

It will be interesting to see how this goes in the next few years. How big can the social media audience get for this account? Would users be willing to pay for such content or special content? How much content could there be? Will a TV show lead to more opportunities or spin-offs or streaming shows? Can Zillow Gone Wild be its own brand soon with different content and products?

Buffalo, New York is projected to be the hottest housing market of 2024, according to an analysis from real estate company Zillow.

Zillow called affordability the “most powerful force driving real estate,” bringing lower-cost markets in the Great Lakes, Midwest and South regions to the top of the company’s 2024 rankings.

“Housing markets are healthiest where affordable home prices and strong employment are giving young hopefuls a real shot at buying and starting to build equity,” said Anushna Prakash, data scientist for Zillow Economic Research…

According to Zillow’s analysis, Buffalo has the highest number of new jobs per home permitted – a measure of expected demand, as new jobs often mean new residents.

The key seems to be the expected job growth in Buffalo. Yes, there is cheaper housing in the region but a growth in jobs means more people which means more demand for housing. How many people would choose a job in Buffalo because of the cheaper housing instead of going elsewhere where housing would be more expensive?

On the list of the predicted top ten housing markets are 6 regions in the Midwest or Northeast – the Rust Belt. This includes Buffalo, Cincinnati, Columbus, Indianapolis, Providence, and Cleveland. If this prediction comes true, would this help create more momentum in these places for a brighter future?

For example, Buffalo’s population peaked in 1950 with over 580,000 residents. In the 2020 Census, Buffalo had over 278,000 residents. The metropolitan region peaked in population in 1970. Similarly, Cincinnati (#2 on the predicted list) peaked in population in 1950 and has lost nearly 200,000 residents since (even as the metro area has grown slowly since then).

Tech firms chose the Phoenix area because of its preponderance of cookie-cutter homes. Unlike Boston or New York, the identikit streets make pricing properties easier. iBuyers’ market share in Phoenix grew from around 1 percent in 2015—when tech companies first entered the market—to 6 percent in 2018, says Tomasz Piskorski of Columbia Business School, who is also a member of the National Bureau of Economic Research. Piskorski believes iBuyers—Zillow included—have grown their share since, but are still involved in less than 10 percent of all transactions in the city…

Barton told analysts that the premise of Zillow’s iBuying business was being able to forecast the price of homes accurately three to six months in advance. That reflected the time to fix and sell homes Zillow had bought…

In Phoenix, the problem was particularly acute. Nine in 10 homes Zillow bought were put up for sale at a lower price than the company originally bought them, according to an October 2021 analysis by Insider. If each of those homes sold for Zillow’s asking price, the company would lose $6.3 million. “Put simply, our observed error rate has been far more volatile than we ever expected possible,” Barton admitted. “And makes us look far more like a leveraged housing trader than the market maker we set out to be.”…

To make the iBuying program profitable, however, Zillow believed its estimates had to be more precise, within just a few thousand dollars. Throw in the changes brought in by the pandemic, and the iBuying program was losing money. One such factor: In Phoenix and elsewhere, a shortage of contractors made it hard for Zillow to flip its homes as quickly as it hoped.

It sounds like the rapid sprawling growth of Phoenix in recent decades made it attractive for trying to estimate and predict prices. The story above highlights cookie-cutter subdivisions and homes – they are newer and similar to each other – and I imagine this is helpful for models compared to older cities where there is more variation within and across neighborhoods. Take that critics of suburban ticky-tacky houses and conformity!

But, when conditions change – COVID-19 hits which then changes the behavior of buyers and sellers, contractors and the building trades, and other actors in the housing industry – that uniformity in housing was not enough to easily profit.

As the end of the article suggests, the algorithms could be changed or improved and other institutional buyers are also interested. Is this just a matter of having more data and/or better modeling? Could it all work for these companies outside of really unusual times? Or, perhaps there really are US or housing markets around the globe that are more predictable than others?

“Our financial goal is to drive rapid growth at scale with sustained improvement in our profitability,” Opendoor, the industry pioneer, wrote in its letter to shareholders this week. After going public last year, Opendoor has now expanded into more than 40 markets and purchased 8,500 homes in the second quarter, more than any other quarter by almost 50%. The company, which is reportedly searching out a new $2 billion revolving credit facility, also announced this week that it is now willing to purchase the majority of homes in every one of its current markets.

Zillow announced similarly ambitious plans during its recent earnings call. While it bought only 3,800 homes in the second quarter, Zillow is gearing up to scale massively through the rest of 2021, saying that it expects its Homes division to bring in around $1.4-1.5 billion in revenue next quarter, roughly double what the division made this quarter…

iBuyers say that in exchange for money they offer convenience, quickly offering a number to homeowners who, if they accept, can then pick their exact move-out date, avoid showing their home, and use the money to immediately go house hunting. (Zillow says its goal is become a “housing market maker.”)…

Still, it’s difficult to deduce at this early moment whether adding high-tech firms to the real-estate market will be a net positive or negative for the typical American family, said Roberto G. Quercia, a professor of city and regional planning at the University of North Carolina at Chapel Hill. Residential real estate remains the dominant form of wealth for such families, making up roughly 70% of median household net worth, so the answer could have potentially enormous ramifications for the country.

The biggest factor seems to be the marriage of tech capabilities and money. There are other actors in the market who have plenty of cash to use. There are plenty of websites and apps for real estate. Does putting them together offer unparalleled convenience or particular knowledge through algorithms and real estate data?

There are multiple sets of consequences to figure out. As the article notes, it is not clear if these new home selling options benefit consumers. More options or more competition could be good. What do other actors like lenders, developers, and realtors think about this? Additionally, many communities might have concerns about institutional buyers who can leverage technology and scale but do not necessarily have local knowledge or concern about local markets. Could these actions drive up prices beyond what regular buyers could afford?

The rise of online real estate sites and apps. These have been around for years but between Zillow.com, Redfin.com. Realtor.com, Trulia.com, and more, potential sellers and buyers have a lot of easily accessible platforms. These options are now ubiquitous: people can search at any time from any location for any length of time. And now that some online listings have video tours and/or 3D models, viewers can get a good sense of what a property is like without ever getting near it.

COVID-19 adds much to existing patterns. With some people interested in moving out of cities and health risks making it more difficult to see homes, online viewing may be the primary option.

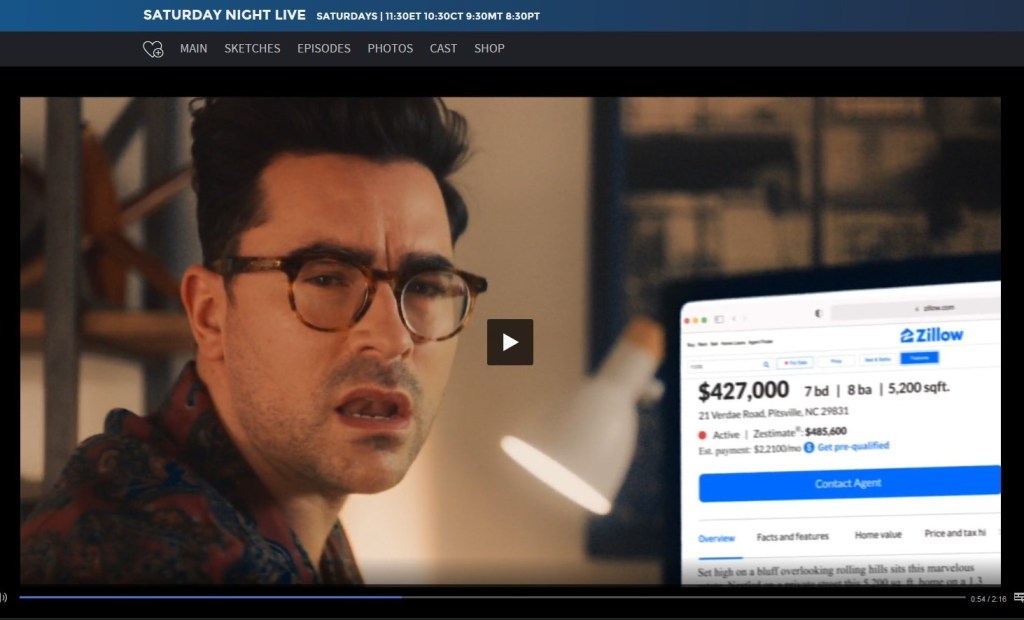

The SNL spoof targeted a particular age group – people in their late-30s – who might be in the middle of a housing dilemma. By this age, those interested in settling down somewhere may or may not have the resources (think school loans, unstable employment during COVID-19 and the last economic crisis in the late 2000s) to buy in the places they want. But, the browsing is free and all sorts of homes in all sorts of locations are available.

Americans also like to consume and compare their social status or possessions to others. With homes occupying such an important part of American mythology, these larger patterns carry over to these sectors. Browsing homes online allows for window shopping and comparisons on one of the most expensive investments. And homes are not just dwellings; they offer windows into lifestyles and neighborhoods.

Put all of these together and you get an SNL reflection on how home searching and purchasing happens today.

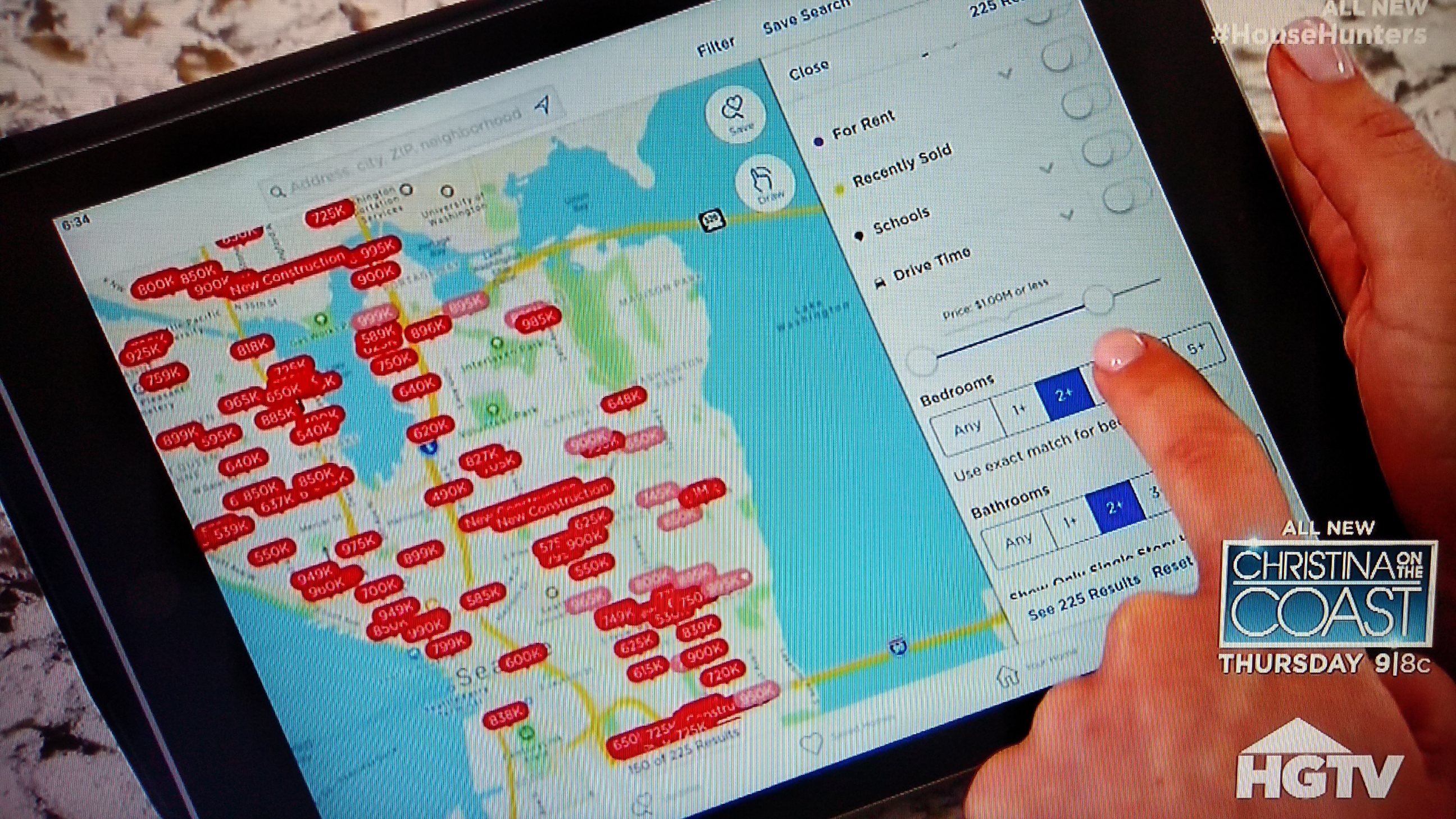

In watching a recent episode of House Hunterson HGTV, I was treated to brief scenes of the couple using Zillow:

Caveats:

-I know this is how people shop for houses today. I have done it myself.

-I would guess this means HGTV and Zillow are working together on the show in some capacity. (See a similar clip on ispotTV.)

-House Hunters tries (!) to show what looking at houses might look like.

Commentary:

Even though the scene was brief, I found it odd. It either seemed like obvious product placement (use Zillow rather than Redfin or MLS or other options!), uninteresting storytelling (watch people look at a screen!), or signaled some major change. As the couple then moved to driving around by themselves and looking at houses, I thought for a short moment that they would not even need a realtor: they had found listings online, arranged their own details, and would tour on their own. (Alas, the realtor just met them at the first house tour.)

While there is a lot of potential for HGTV and other similar programming to incorporate devices and screens (mainly smartphones and tablets) into their portrayals of finding property, there is a bigger issue at play for television and film: how can you interestingly portray handheld screens that so many of us are buried in on a daily basis within a story that has to move at a rapid pace? This is not easy.